How to Understand Your Credit Report

Your credit report gives a detailed look at how you manage money.

Here’s a quick and easy guide to help you understand each section and term so you can take control of your financial future!

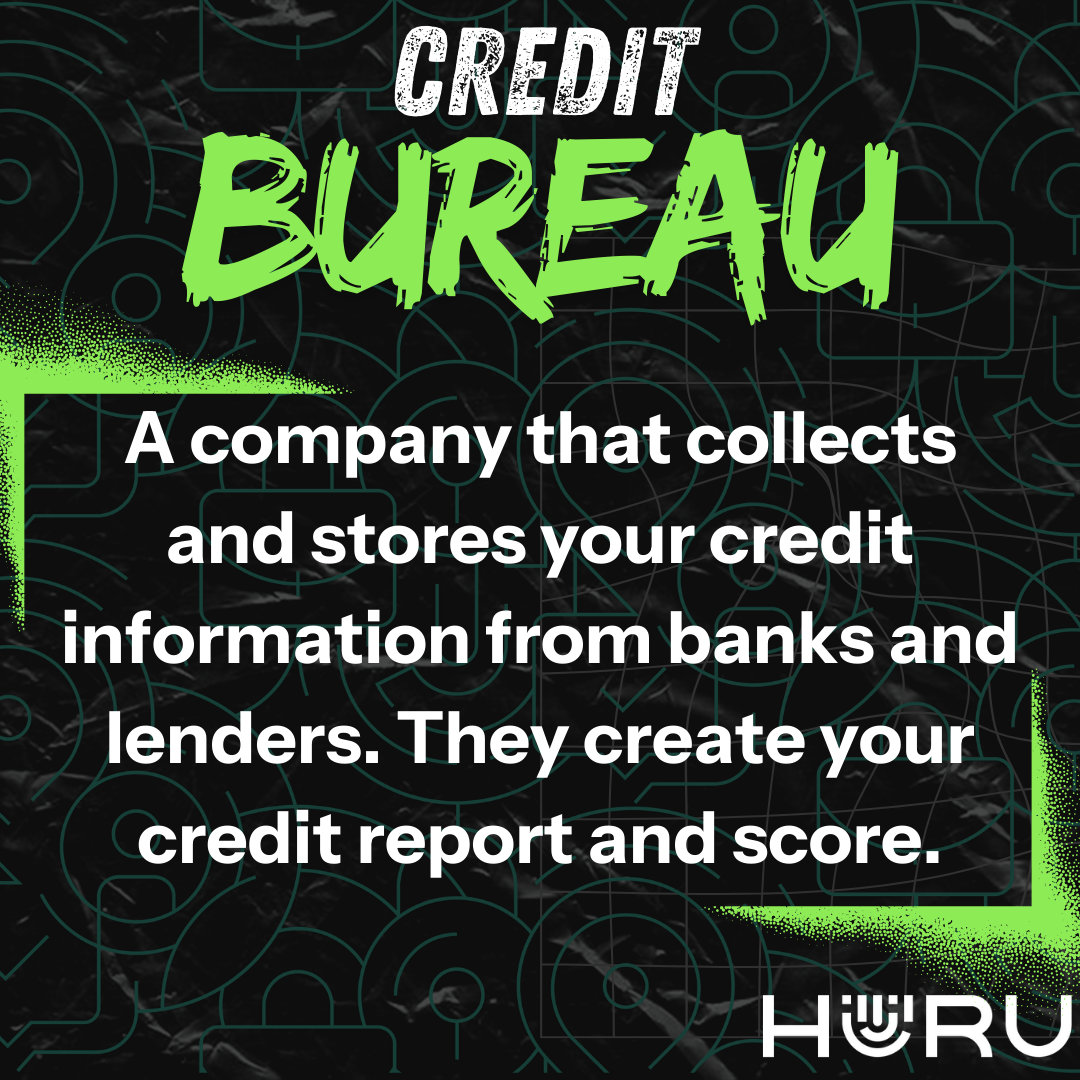

Key Terms in Your Credit Report

Key Applications of Your Credit Report

- Loan and Credit Applications: Lenders use your credit report to determine your creditworthiness. A higher credit score can mean better interest rates and loan terms.

- Renting a Home: Landlords often check credit reports to gauge whether tenants can reliably meet rental payments.

- Employment Opportunities: Some employers assess credit reports as part of their hiring process, especially for roles involving financial responsibility.

- Financial Planning: By reviewing your credit report, you can identify areas for improvement and set goals to enhance your financial standing.

Key Sections of a Credit Report

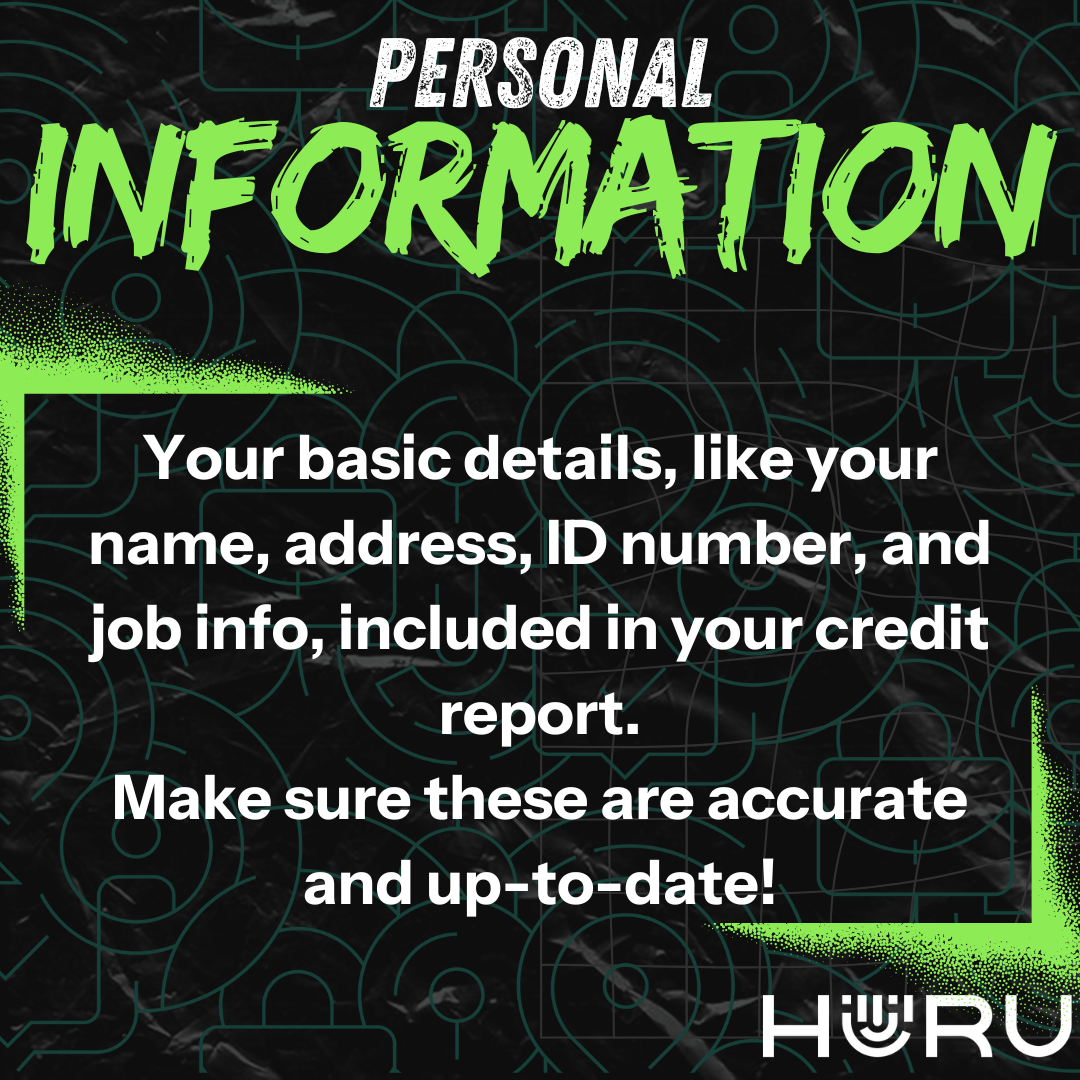

Personal Information

This section confirms your identity and includes:

- Full Name

- ID Number

- Date of Birth

- Contact Details

- Employment Information (if available)

Tip: Check that all personal details are accurate. Mistakes here could lead to mixed-up credit data.

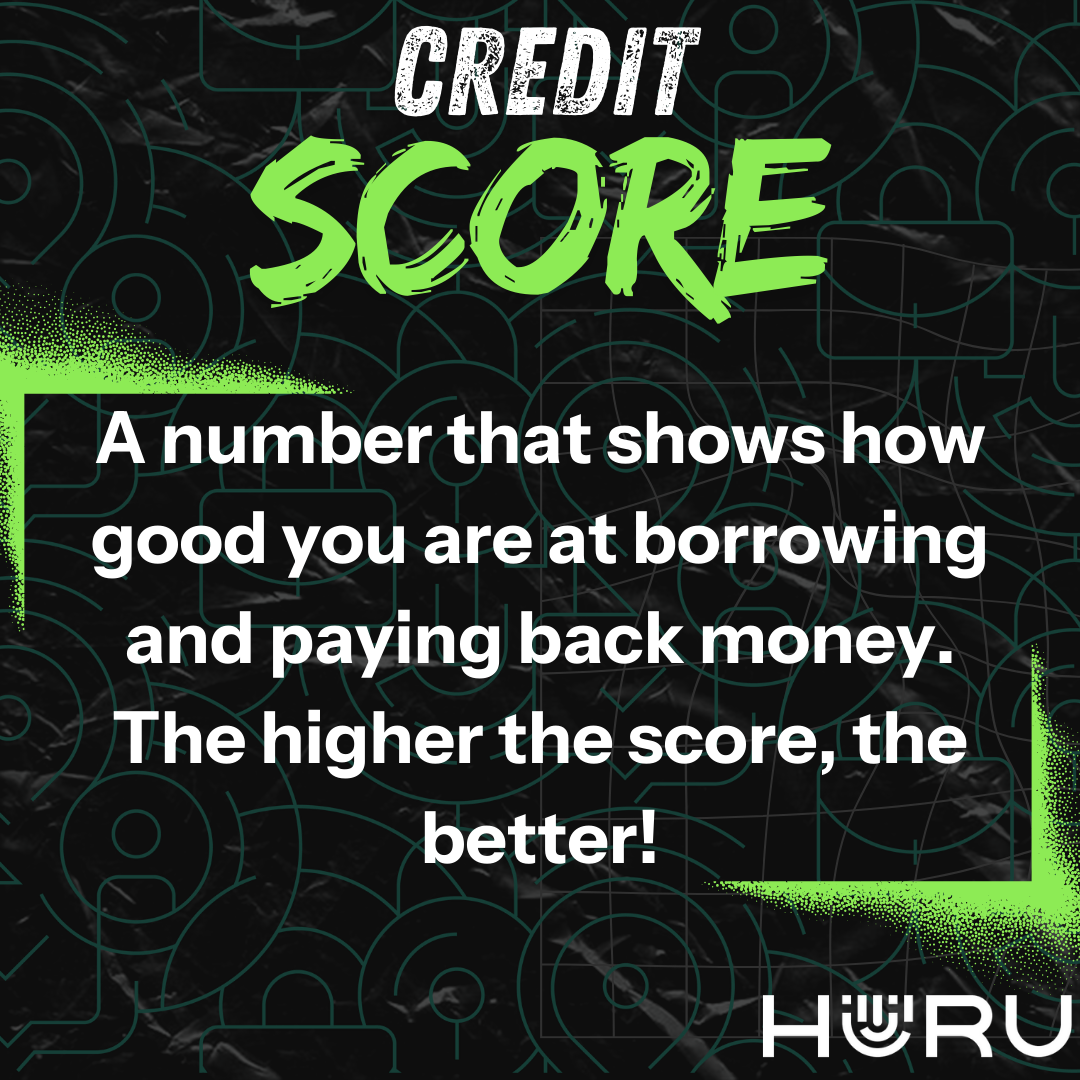

Credit Score

Your credit score is a 3-digit number that summarises your creditworthiness.

| Typical Score | Rating |

| 0-599 | Poor |

| 600-649 | Average |

| 650-699 | Good |

| 700-749 | Very Good |

| 750-850 | Excellent |

Tip: The higher your score, the better your chances of being approved for credit with favourable terms.

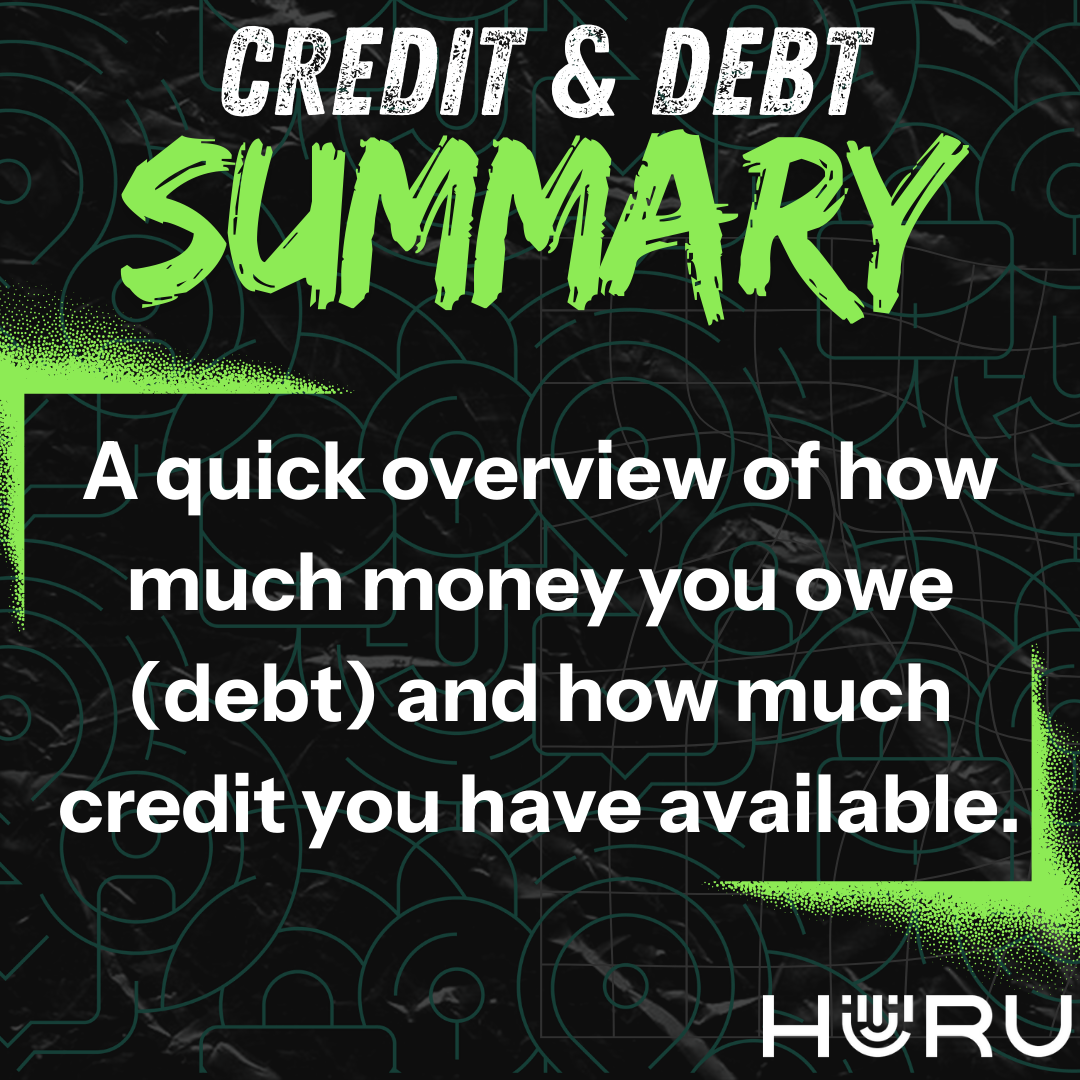

Accounts / Trade Lines

This section lists all your credit accounts – such as store cards, loans, and credit cards – with details such as:

- Lender Name

- Account Type

- Opened Date

- Balance Owed

- Credit Limit

- Payment History

Look for:

- “Current” or “Up to date” – Good standing

- “In arrears” – Payments are behind

- “Written off” – Lender gave up collecting the debt

- “Charged off” – Similar to written off; affects your score

Payment History

A detailed view of how you’ve paid each account over time. Usually shown as a monthly history:

- On Time

- Late or Missed

- Default

Tip: Consistent on-time payments improve your credit profile.

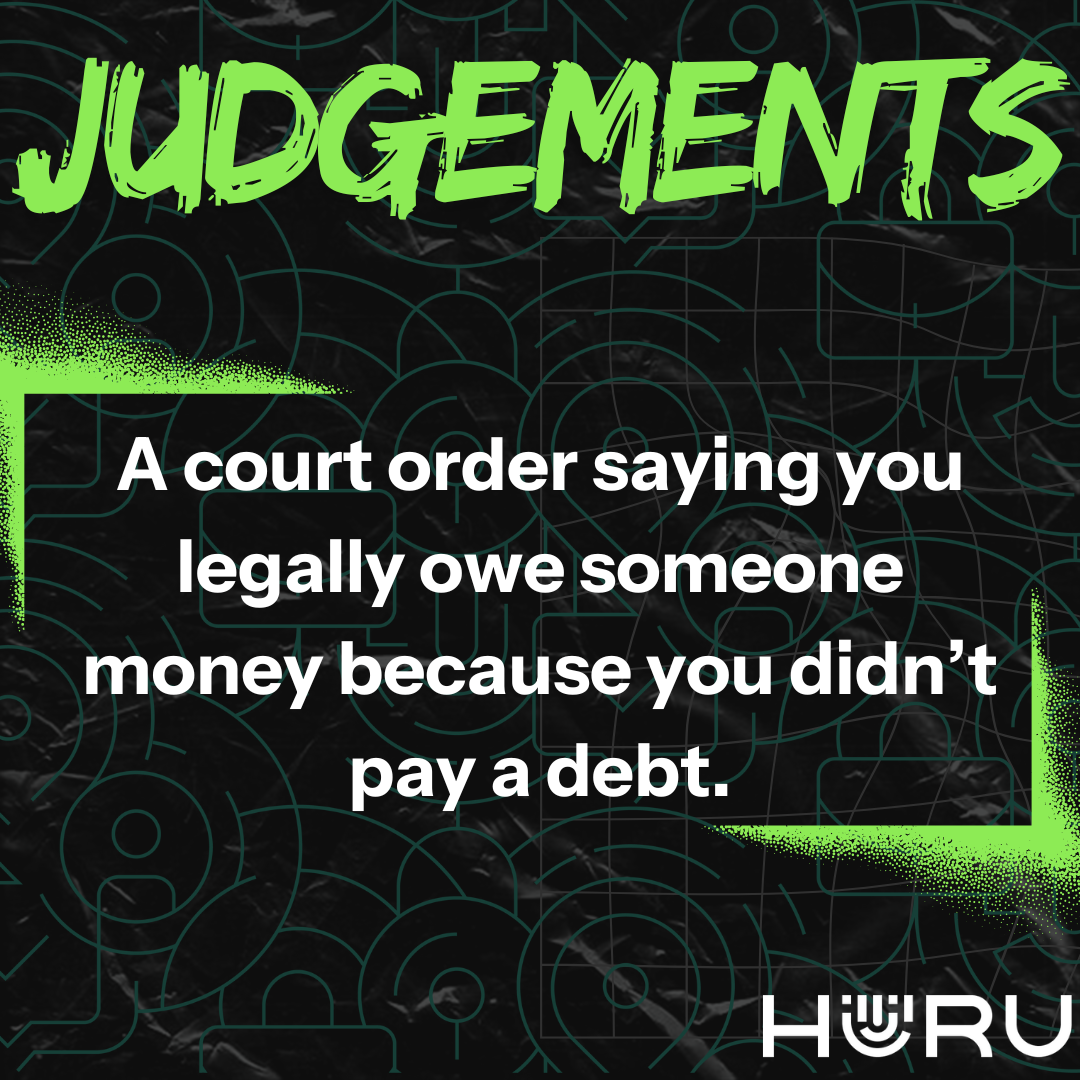

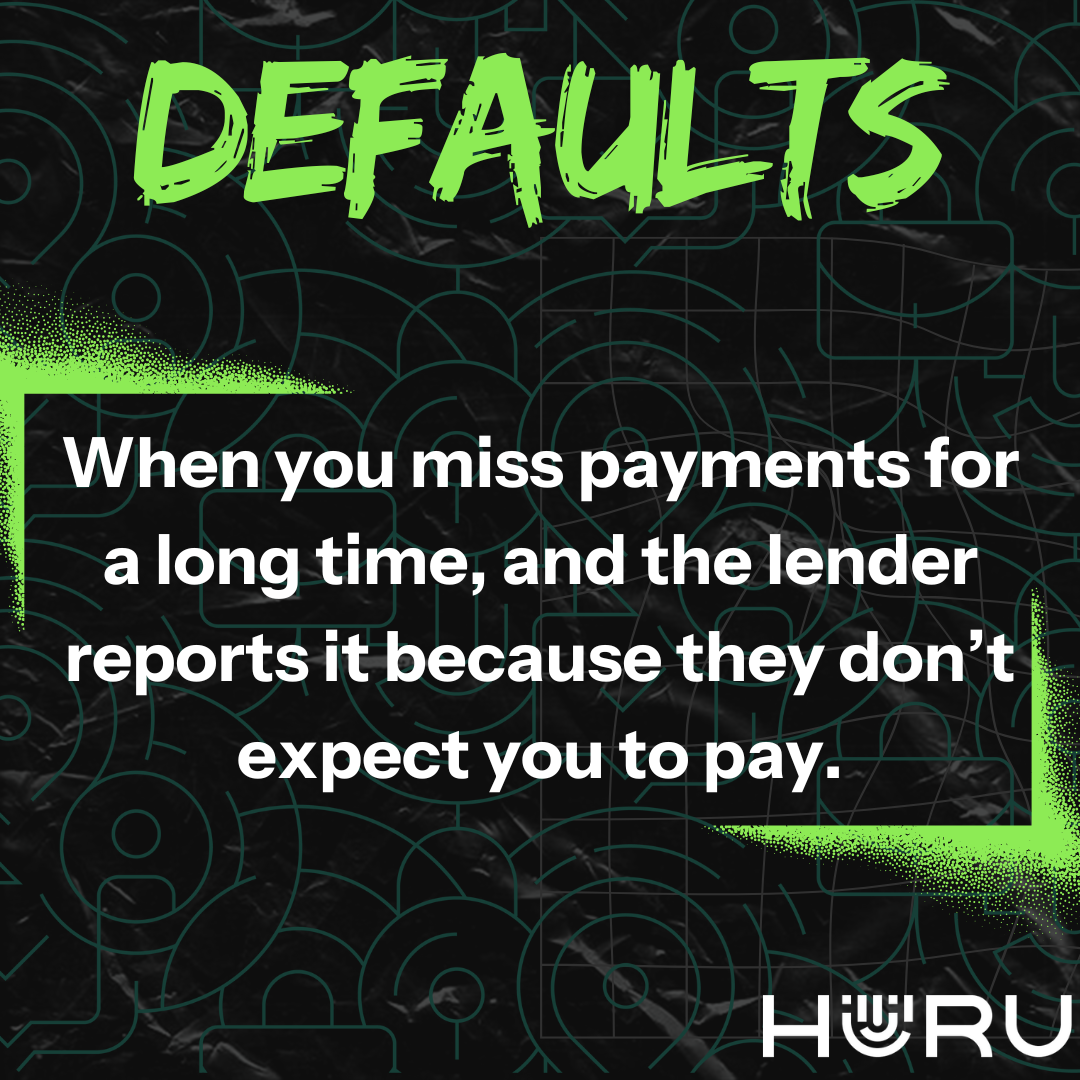

Judgments and Defaults

This section flags any serious credit events:

- Judgments: Legal decisions requiring you to pay a debt

- Defaults: Credit providers marked your account as not repaid as agreed

- Enquiries by Debt Collectors

These remain on your report for up to five years, even if paid off.

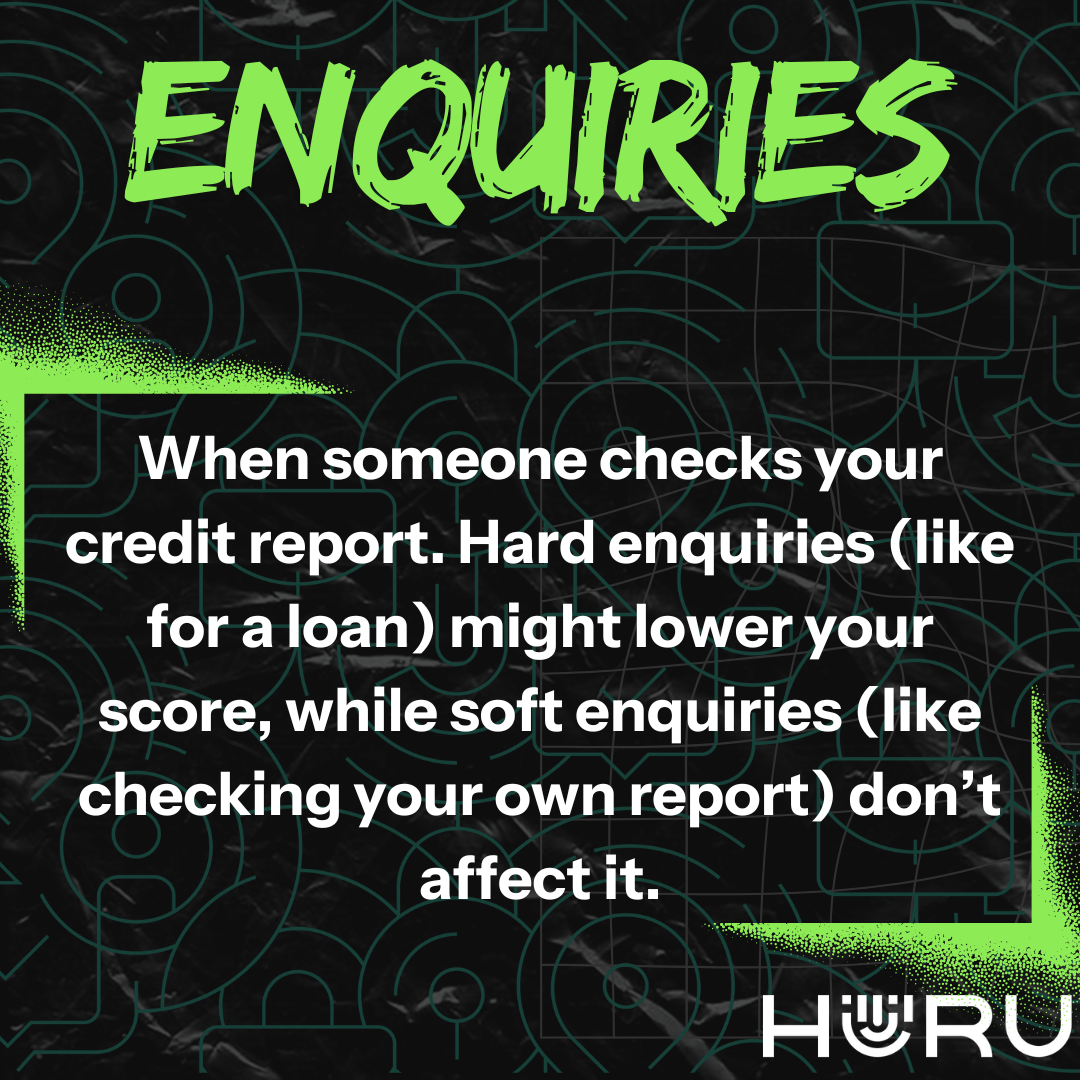

Enquiries (Searches)

Shows who has accessed your credit report recently:

- Soft Enquiry: You checked your own report (no impact on score)

- Hard Enquiry: A credit provider reviewed your report for a loan or product (can affect score)

Tip: Too many hard enquiries in a short time may signal risk to lenders.

Common Terms Explained

| Term | Meaning |

| Arrears | Missed payment |

| Default | Loan account marked as unpaid after repeated missed payments |

| Judgement | Legal ruling that you owe money |

| Credit Limit | Maximum amount you can borrow on a specific account |

| Outstanding Balance | How much you still owe |

| Credit Provider | Bank or institution giving you credit |

| Debt Review | A legal process to assist with over-indebtedness |

| Settlement | Agreement to pay off a debt, usually at a reduced amount |

What to Do If You Spot Errors

- Verify your identity and account information

- Report incorrect entries to the credit bureau (e.g. TransUnion, Experian, VCCB, XDS,)

- Provide supporting documents like ID or proof of payment

- The credit bureau must investigate within 20 business days

Quick Tips to Maintain a Healthy Credit Profile:

- Pay your accounts on time every month

- Keep your credit utilisation below 30%

- Avoid applying for too much credit at once

- Check your report annually for errors

Questions?

If you’re using HURU to access your credit report, reach out to us – We’ll help you understand your report and guide you on next steps!